12/22/24

Weekly Market Recap

Last week was marked by some volatility following Jerome Powell’s press conference on Wednesday. Although the Federal Reserve lowered interest rates by another 25 basis points, Powell indicated that there would be fewer rate cuts in 2025 than previously expected. The S&P 500 fell by about 3% immediately after the press conference and continued to decline through Wednesday’s market close. However, positive economic data released on Thursday and Friday helped stocks recover some of those losses. Notably, the US Leading Economic Index increased for the first time in two years, suggesting that economic activity is likely to improve over the next six months. Additionally, the Federal Reserve’s preferred measure of inflation (PCE Index) rose by only 0.1% in November, bringing the year-over-year rate to 2.4%. This week will be shortened due to the holidays, with markets closing early on Christmas Eve and fully closed on Christmas Day. After that, only four more trading days remain in 2024. Barring any major disruptions, 2024 is set to be a standout year for stocks.

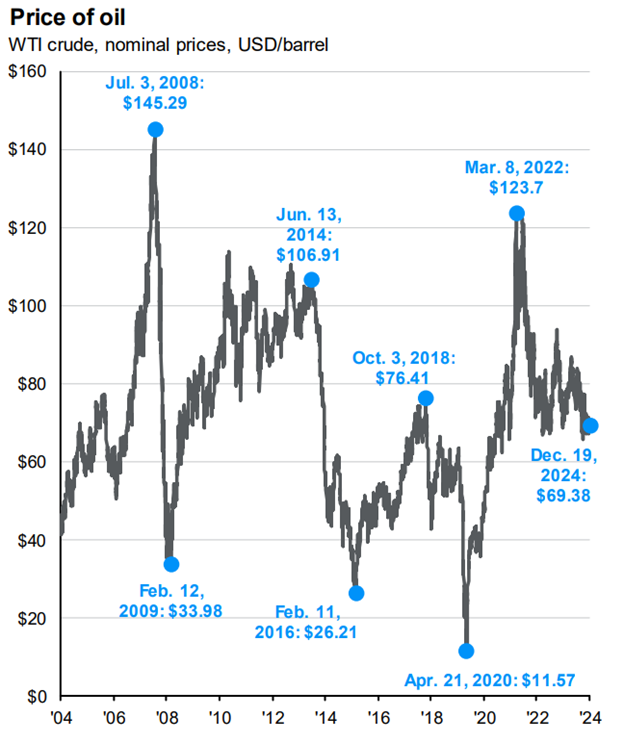

Chart of the Week

This week’s chart illustrates the price of oil over the past 20 years. As the chart shows, oil is a highly volatile commodity, with prices rising or falling sharply over short periods. It’s somewhat surprising that oil prices remain well below their 2008 peak. The chart is not adjusted for inflation, and even in nominal terms, oil is cheaper today than it was in 2008. If inflation were factored in, the drop in oil prices since 2008 would appear even more significant. This decline is the primary reason why the energy sector of the stock market has dramatically underperformed the S&P 500 over the past decade. In fact, energy stocks have lagged the broader market by nearly 180% over the last ten years. By contrast, during the previous decade (December 2004 to December 2014), energy stocks outperformed the broader market by roughly 47%.

Written by:

Ben Rones, CFA®

Senior Analyst at R&R Financial

The commentary in this newsletter is for informational purposes only and should not be taken as personalized investment adviceChart of the week Source: J.P. Morgan Asset Management; (Top and bottom left) EIA;(Right) FactSet; (Bottom left) Baker Hughes.*Forecasts are from the November 2024 EIA Short-Term Energy Outlook andstart in 2024. **U.S. crude oil inventories include the Strategic PetroleumReserve (SPR). Liquid fuels include crude oil, natural gas, biodiesel and fuelethanol. Active rig count includes both natural gas and oil rigs. WTI crudeprices are continuous contract NYM prices in USD. Guide to the Markets – U.S.Data are as of December 19, 2024.